Best Personal Loan Options for Bad Credit

Finding a lender willing to approve a personal loan with bad credit can initially feel like a relief. After multiple denials or restrictive conditions, many borrowers focus mainly on approval and stop paying attention to how the repayment structure may affect their finances later.

This is where many financial problems quietly begin. Longer repayment terms, higher APR rates, and additional fees may increase the total borrowing cost far more than expected over time.

Understanding how lenders evaluate financial profiles may help borrowers identify which loan conditions deserve more attention before applying.

Different lenders may also evaluate financial profiles very differently. Because of that, understanding how loan structures work before accepting any offer may help borrowers avoid financial decisions that create additional pressure later.

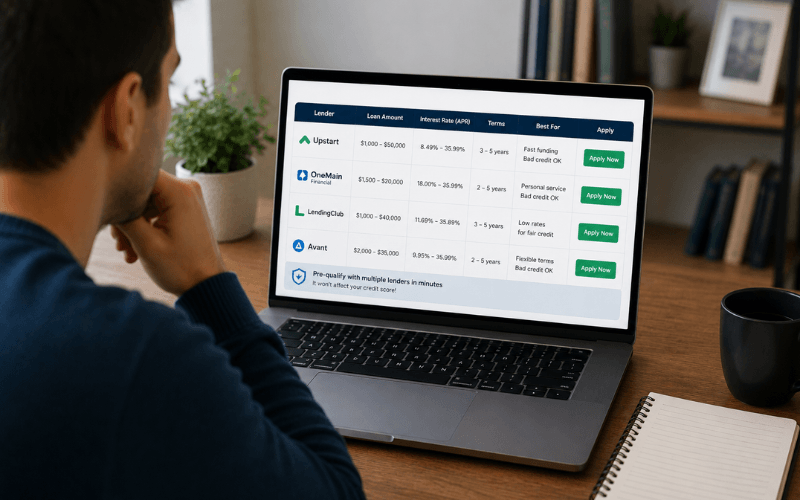

📋 Why loan offers may look completely different for borrowers with bad credit

Borrowers with lower credit scores often notice that loan conditions vary significantly between lenders. Some institutions focus heavily on credit score, while others may evaluate additional factors such as income stability, payment consistency, and current debt obligations.

This is one reason similar financial profiles sometimes receive completely different loan offers. One lender may offer longer repayment terms with higher interest rates, while another may focus more on monthly affordability.

APR rates also tend to increase when lenders identify higher repayment risk. Because of that, borrowers with lower scores frequently receive more restrictive borrowing conditions compared to applicants with stronger financial profiles.

Understanding these differences helps borrowers compare loan structures more carefully instead of focusing only on immediate approval.

Different repayment structures may affect the total loan cost much more than many borrowers initially expect.

💳 Explore Loan Options

Some borrowers choose to compare loan options from multiple lenders before making a final decision. Reviewing different offers may help identify repayment conditions that fit better financially.

Loan options

Go to the official website to view options and apply if it fits your needs

Visit the official website to start your application.

You will be redirected to the official provider.

This is an independent informational page and is not affiliated with the provider.

Always review terms and conditions before applying.

💰 Lower monthly payments do not always mean a better loan option

Many borrowers naturally pay attention to the monthly payment amount first. Smaller payments may look more manageable during financially stressful situations, especially when immediate financial relief becomes the priority.

However, lower monthly payments sometimes come attached to longer repayment periods. As interest continues accumulating over time, the total amount repaid may become much higher than expected.

This is why reviewing APR, repayment length, and total repayment estimates often becomes more important than focusing only on short term affordability.

In some situations, borrowers may accept a loan that initially feels easier to manage while unknowingly increasing long term financial pressure.

⚠️ Financial urgency may lead borrowers to ignore long term repayment pressure

When financial stress becomes overwhelming, many people focus entirely on finding immediate approval. This often happens after dealing with missed payments, rising balances, or increasing monthly obligations.

During these situations, borrowers sometimes accept the first available offer without carefully analyzing the long term impact of the repayment structure itself.

High interest rates combined with multiple existing debts may create even more pressure later, especially when credit card balances and loan payments start overlapping at the same time.

For some borrowers, reorganizing existing debt may become just as important as getting approved for a new loan.

Managing several balances with high interest rates at the same time may gradually increase financial pressure.

📈 Small financial adjustments may gradually improve future borrowing conditions

Improving loan conditions does not always require immediate major financial changes. In many situations, small adjustments in financial habits may slowly strengthen how lenders evaluate borrowing risk.

Reducing revolving balances, avoiding missed payments, and maintaining more organized financial activity often help create healthier borrowing conditions over time.

Even when credit score improvements happen gradually, stronger financial organization may positively affect future applications and repayment opportunities later.

Borrowers who understand how financial behavior influences lending decisions often make more sustainable borrowing choices instead of focusing only on short term approval.

Improving financial habits gradually may help strengthen approval conditions and reduce borrowing difficulties over time.

🏦 What borrowers should evaluate before accepting any loan offer

Approval alone should never be the only factor considered during the borrowing process. Understanding the full repayment structure usually helps borrowers make safer financial decisions.

APR remains one of the most important details because it reflects the yearly borrowing cost more accurately than interest rate alone. Additional fees may also affect the total loan cost depending on the lender and repayment structure involved.

Repayment length matters as well. While longer terms may reduce monthly pressure temporarily, they sometimes increase the total amount paid substantially over time.

Reviewing these conditions carefully before accepting any agreement helps borrowers better understand the long term financial impact involved.

🧩 Understanding loan structures more clearly may help create safer financial decisions

Borrowers dealing with lower credit scores often face more restrictive financial conditions, which makes careful comparison even more important before accepting any loan offer.

Interest rates, repayment terms, existing debt, and overall financial organization all influence how manageable a loan may become over time.

The more clearly borrowers understand how repayment structures affect long term financial costs, the easier it becomes to identify borrowing options that fit their financial situation more responsibly and sustainably.

Frequently Asked Questions About Bad Credit Personal Loans

Can someone still qualify for a personal loan with bad credit?

Yes. Some lenders analyze several financial factors beyond credit score alone. Income stability, payment consistency, and debt levels may also influence approval decisions.

Different institutions use different approval models, which means borrowing conditions may vary significantly between lenders.

Why are interest rates usually higher with bad credit?

Lenders often increase interest rates when they identify greater repayment risk. Lower scores sometimes indicate previous financial difficulties, missed payments, or higher debt utilization.

Because of that, borrowers with lower scores frequently receive more restrictive borrowing conditions.

Does comparing multiple lenders really matter?

Yes. Loan structures, repayment terms, fees, and APR rates may differ considerably even for similar financial profiles.

Comparing multiple offers carefully helps borrowers better understand the total borrowing cost instead of focusing only on approval speed.

Can financial habits improve future loan conditions?

In many situations, yes. More organized financial behavior may gradually influence how lenders evaluate repayment risk.

Reducing revolving balances and maintaining more stable payments often help strengthen future borrowing opportunities.

Why do many borrowers with bad credit also research debt consolidation?

High interest balances and multiple monthly payments often create financial pressure that becomes difficult to manage over time.

Some borrowers begin researching consolidation strategies as a way to simplify repayment structures and improve financial organization.

Understanding how repayment conditions work before accepting any agreement remains extremely important regardless of the borrower’s current financial profile.