How to Compare Personal Loan Options Online

Searching for a personal loan online often starts with a simple goal. You want to check rates, understand your options, and find something that fits your situation. A few minutes later, dozens of lenders, offers, and payment estimates start appearing everywhere.

Some loans promise lower monthly payments, while others focus on fast approval or flexible terms. At first, many offers seem similar, which makes the decision feel more confusing than expected.

The problem is that choosing based only on the first attractive number can become expensive later. Understanding what actually matters before accepting an offer is what helps you avoid unnecessary costs and make a smarter financial decision.

🚀 What you should compare before choosing a personal loan

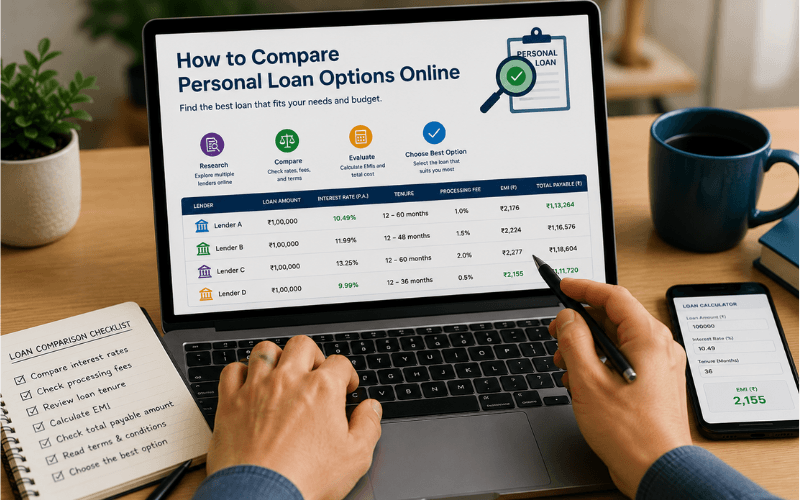

One of the first things to compare is the APR, which represents the total yearly borrowing cost. Many users focus only on the monthly payment and ignore how much the loan will really cost over time.

The repayment term also matters more than most people expect. Longer terms usually reduce monthly payments, but they may significantly increase the total amount paid in interest.

Another important point is checking fees. Some lenders charge origination fees, late payment penalties, or additional costs that are not obvious at first glance.

You should also compare the total repayment amount, not only the installment value. A loan with smaller payments may still become more expensive in the long run.

Looking at these details together gives you a much clearer understanding of which offer actually fits your financial situation.

⚠️ Why the lowest monthly payment is not always the best option

Lower monthly payments often look safer and easier to manage. However, smaller installments sometimes hide longer repayment periods and higher total interest costs.

For example, extending a loan for several extra years may reduce the monthly amount, but it can also increase the total repayment significantly over time.

This is one of the reasons why comparing only the monthly payment can become misleading. The real financial impact usually appears when you calculate the full loan cost from beginning to end.

Understanding this helps you avoid choosing a loan that feels comfortable now but becomes much more expensive later.

Learn what may positively affect your credit score before applying for a loan.

💡 How online loan comparison helps you make better decisions

Online comparison tools make it easier to review multiple loan offers without immediately committing to one lender. This creates a safer environment for evaluating rates, terms, and overall conditions more carefully.

Comparing options before applying also helps reduce emotional decisions. Instead of rushing into the first available offer, you gain a better understanding of what is actually available for your financial profile.

Another advantage is visibility. Some lenders work better for users with stronger credit profiles, while others may offer more flexible conditions for borrowers with average scores.

Taking time to compare first usually leads to more financially sustainable decisions and helps avoid unnecessary borrowing costs later.

💳 Some lenders offer more flexible conditions than others

Different lenders evaluate financial profiles differently, which means loan conditions can vary significantly from one provider to another.

💳 LendingClub

LendingClub is known for offering online personal loan options with flexible conditions for different financial profiles. It is often used by borrowers looking to compare rates online.

👉 View options: https://www.lendingclub.com/

You will be redirected to the official provider

This is an independent informational page and is not affiliated with the provider.

Always review terms and conditions before applying.

💳 Upstart

Upstart evaluates more than traditional credit factors and may offer different approval opportunities depending on the financial profile being analyzed.

👉 View options: https://www.upstart.com/loans

You will be redirected to the official provider

This is an independent informational page and is not affiliated with the provider.

Always review terms and conditions before applying.

Comparing multiple lenders instead of focusing on only one option usually gives you a better understanding of available conditions and possible costs.

📊 How your financial profile changes the offers you receive

Loan offers are heavily influenced by your financial profile. Two people applying for similar amounts may receive completely different rates and conditions based on their credit history and financial behavior.

Credit score is one of the strongest factors lenders analyze. Higher scores usually increase approval chances and may also improve interest rates.

Debt levels also affect the decision. Lower balances generally create stronger borrowing conditions because lenders view the profile as less risky.

Income stability is another important point. Consistent earnings and organized finances often create more confidence during loan evaluations.

Because of that, improving your financial profile before applying can directly affect the quality of the offers you receive.

Here’s what you can do to increase your chances of loan approval.

🧠 What to review before accepting any loan offer

Before accepting any loan, it is important to review the complete terms carefully instead of focusing only on approval speed.

Checking the final APR helps you understand the real borrowing cost. Reviewing repayment terms also helps avoid financial pressure later.

It is also important to look for hidden fees, early repayment penalties, and additional conditions that may increase the total loan cost over time.

Reading the details carefully may seem slow at first, but it often prevents expensive financial mistakes later.

The more clearly you understand the offer, the easier it becomes to choose a loan that actually supports your financial situation.

🚀 Why comparing first usually leads to better financial choices

Financial decisions become safer when they are made with more information and less urgency. Comparing personal loan options before applying gives you more control over the process and reduces the risk of accepting unfavorable conditions.

Better comparisons often lead to lower long term costs, healthier payment structures, and more confidence when borrowing money.

Instead of focusing only on getting approved quickly, understanding the differences between lenders helps you make choices that fit your financial reality more effectively.

A personal loan can become a useful financial tool when chosen carefully. The more attention you give to comparison and preparation now, the easier it becomes to avoid unnecessary costs and make stronger financial decisions in the future.