How to Consolidate Credit Card Debt With a Personal Loan

One balance starts growing, another payment date appears, and after a while a large part of the monthly budget begins disappearing into interest charges. Even when payments are made consistently, the total debt sometimes feels like it barely changes.

This situation becomes even more stressful when different cards have different APR rates, minimum payments, and due dates. Financial organization gets harder, and many users start feeling trapped in a cycle where interest continues growing faster than expected.

Learn what may positively affect your credit score before applying for a new card.

Because of that, debt consolidation becomes an option many borrowers start researching when trying to simplify payments and regain more financial control. Replacing multiple balances with a more organized repayment structure may help reduce the confusion caused by several monthly due dates and different interest rates. In some situations, it may also create more predictable financial conditions and make long term budgeting easier to manage.

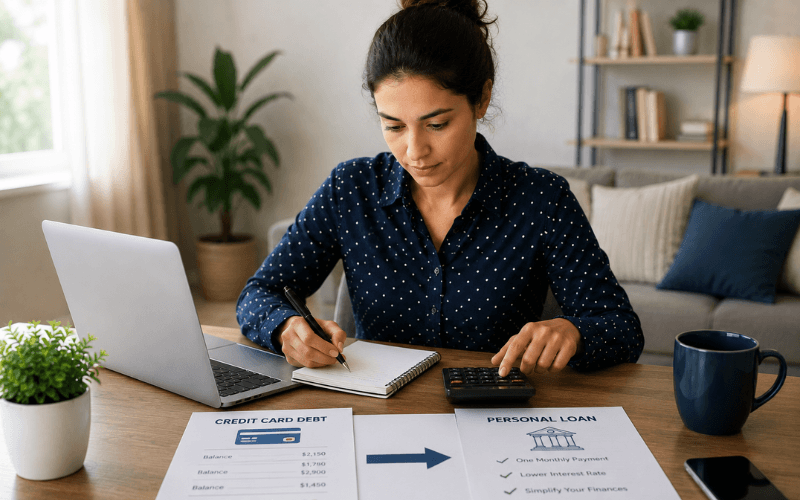

🏦 How debt consolidation with a personal loan usually works

Debt consolidation normally means using a personal loan to combine multiple credit card balances into one structured payment. Instead of managing several separate accounts every month, the borrower focuses on a single repayment plan.

For some users, this may help create more predictable monthly expenses and improve financial organization. In certain situations, the interest rate attached to the personal loan may also be lower than the APR charged by revolving credit card balances.

Another advantage is clarity. A structured repayment term makes it easier to understand how long repayment may take compared to ongoing revolving balances that continue generating interest every month.

However, consolidation does not automatically solve financial pressure by itself. The loan conditions and the financial habits that follow after consolidation still play a major role in the long term result.

Learn what may positively affect your credit score before applying for a new card.

📉 Why revolving credit card balances often become expensive over time

Credit card debt becomes difficult to manage mainly because revolving balances continue generating interest repeatedly. Even relatively small balances can grow much faster than expected when high APR rates remain active month after month.

In many situations, minimum payments reduce only a small portion of the original debt while most of the payment goes toward interest charges. This creates the feeling that repayment is happening very slowly despite regular monthly payments.

Using multiple cards at the same time may increase this pressure even more. Different due dates and separate balances can make budgeting harder and reduce visibility into the total financial situation.

Understanding how revolving debt works is important before considering any consolidation strategy.

💰 When consolidation may help improve financial organization

For borrowers struggling with multiple payment schedules, consolidation may help simplify the financial structure into one organized repayment plan.

Instead of tracking several credit card accounts separately, one structured payment may create more predictability and reduce some of the stress connected to financial management.

In some cases, borrowers also use consolidation as a way to create a clearer repayment timeline. Knowing exactly when the debt may be fully repaid often feels easier than managing revolving balances without a defined end date.

Financial organization is usually one of the biggest advantages people look for when considering debt consolidation.

📋 Why minimum payments sometimes keep debt growing longer

Minimum payments may create temporary short term relief, but they often extend repayment for much longer periods than borrowers initially expect.

Because interest continues accumulating, paying only the minimum amount sometimes causes balances to decrease very slowly over time. This is one of the reasons many users remain in debt for years even while making regular monthly payments.

The longer high interest balances remain active, the more expensive the total repayment may become. Small differences in APR can significantly affect the final borrowing cost during long repayment periods.

Understanding this helps borrowers evaluate whether restructuring debt may create better long term financial conditions.

🔍 What to compare before choosing any consolidation strategy

Before applying for a consolidation loan, reviewing the complete repayment structure carefully is extremely important. Lower monthly payments alone do not always mean the overall loan will cost less.

APR should always be analyzed because it helps clarify the real yearly borrowing cost. Repayment length also matters because longer terms may increase the total amount paid over time even when monthly payments appear smaller.

Additional fees may also affect the total cost significantly depending on the lender and repayment structure involved.

Comparing the full financial impact instead of focusing only on short term monthly relief usually leads to more informed borrowing decisions.

🧠 Why spending habits still matter after consolidation

Debt consolidation may reorganize existing balances, but financial habits still determine what happens after the new repayment structure begins.

Continuing to rely heavily on revolving credit cards while also managing a consolidation loan may create additional financial pressure later. This is why many financially stable borrowers focus not only on repayment, but also on improving spending control and budgeting habits over time.

Small adjustments in daily financial behavior often create stronger long term improvements than short term financial solutions alone.

Building healthier financial habits after consolidation usually increases the chances of maintaining better financial stability in the future.

📈 Better financial decisions often begin with clearer financial visibility

Many debt problems become more manageable once the full financial situation becomes easier to understand. Reviewing balances carefully, understanding repayment costs, and creating more organized payment structures often reduce financial stress significantly.

Debt consolidation may help simplify repayment for some borrowers, especially when the goal is improving organization and creating more predictable financial conditions.

The more clearly you understand how interest, repayment terms, and financial habits affect long term costs, the easier it becomes to make safer borrowing decisions and gradually build a stronger financial profile over time.